This post contains affiliate links. If you click and make a purchase, I may receive a small commission at no extra cost to you. Thank you for supporting the site!

Compare YNAB vs Personal Capital for personal finance tools tracking. Find which budgeting app fits your lifestyle, income type, and financial goals in 2025.

Utilizing finance tools effectively can enhance your budgeting experience.

Many people find that finance tools simplify complex financial tasks.

Both finance tools serve unique purposes in managing money.

For effective budgeting, exploring different finance tools is essential.

Choosing the right finance tools can significantly impact your financial health.

Employing finance tools can help you visualize your spending patterns.

Both finance tools offer unique insights into your financial behavior.

Effective finance tools can prevent overspending and improve budgeting.

Using finance tools to track expenses is crucial for financial health.

Finance tools play a vital role in managing your financial life effectively.

Deciding between finance tools should consider your financial goals.

Evaluating finance tools can lead to better financial decisions.

Finding the right finance tools aligns with your financial habits.

Finance tools should match your income style for optimal results.

Different finance tools cater to diverse financial situations and needs.

Many finance tools help facilitate wealth building and spending tracking.

Finance tools can be tailored to suit individual financial journeys.

Researching various finance tools will yield beneficial insights.

Picking between paid and free personal finance tracking tools feels like a financial decision in itself. You see YNAB’s $109 annual subscription and wonder if it’s worth the cost.

Finance tools enable you to create actionable financial plans effectively.

Incorporating finance tools can help streamline your financial processes.

Finance tools provide essential data for smarter financial strategies.

Many finance tools can help visualize expenditures and savings.

Adopting finance tools is key for proactive financial planning.

The right finance tools can empower you to manage your budget effectively.

Finance tools enable users to track their financial progress accurately.

Leveraging finance tools can support long-term financial goals.

Finance tools are essential for identifying savings opportunities.

Using finance tools leads to better money management choices.

Many finance tools help clarify your financial decisions.

Finance tools can guide you to better understanding of your finances.

Both finance tools allow for comprehensive financial analysis.

Understanding the differences between free and paid finance tools is essential for making the right choice for your personal finances.

Then you look at Personal Capital’s free dashboard and think you’ve found the perfect solution.

The choice gets harder when you consider what each platform actually does. YNAB forces you to assign every dollar before you spend it.

Personal Capital shows you where your money went after the fact.

One needs daily attention. The other runs on autopilot.

The real cost isn’t always the subscription price. You might waste more money from financial blindness than you’d ever spend on the right tool.

Missing expense patterns costs money.

Paying hidden investment fees costs money. Managing everything in spreadsheets burns you out, and that costs money too.

Overview: Why Your Choice Changes Everything

Choosing the Right Finance Tools for Your Needs

Most people pick financial tools based on features or price. That’s backwards.

You need to pick based on how you actually earn money and make decisions.

A freelancer with irregular income needs different tools than a salaried couple. Someone building wealth needs different insights than someone getting out of debt.

A recent graduate establishing independence needs different structure than an experienced professional optimizing investments.

YNAB and Personal Capital (now operating as Empower) have moved in opposite directions over the years. They don’t compete anymore because they solve different problems for different people.

Understanding which problem you actually have saves you from switching platforms six months from now after wasting time learning the wrong system.

Feature Comparison: What Each Platform Actually Does

YNAB’s Budget-First Approach

YNAB operates on zero-based budgeting. Every dollar that comes in gets assigned to a specific category before you spend it.

This isn’t theoretical planning.

You literally categorize your income into budget categories, and the app tracks whether you’re staying within those assignments.

The system works through what YNAB calls “giving every dollar a job.” When money hits your account, you decide what it needs to do before your next paycheck arrives. What bills need paying?

What larger expenses are you saving for?

What goals matter most right now?

This needs engagement. You can’t set it and forget it.

The customization runs deep. You create category groups that match your actual spending patterns.

A freelancer might organize categories around different client projects and business expenses.

A couple might separate shared household costs from personal discretionary spending. Someone paying off student loans might focus heavily on debt paydown categories.

Personal Capital’s Wealth-Tracking Focus

Personal Capital (rebranded as Empower) takes the opposite approach. The free dashboard consolidates all your financial accounts into one view.

Checking accounts, savings, credit cards, loans, investments, and retirement accounts all show up in a single interface.

The budgeting tools here are basic compared to dedicated budget software. You can set spending targets and watch categories, but it’s reactive.

You’re watching your spending after it happens, not planning it before.

The platform shines when showing your finish financial picture. Total net worth.

Portfolio balance.

Retirement savings progress. Emergency fund status.

Debt paydown timeline.

Empower’s investment tools separate it from typical personal finance tracking tools. The Investment Checkup analyzes your portfolio, flags hidden fees, and offers allocation recommendations.

Most people don’t know they’re overpaying on investment fees until something like this points it out.

Automation Differences

YNAB needs 20-30 minutes from you each month after initial setup. Transactions import automatically and categorize based on previous entries, but you’re reviewing them and confirming assignments.

The system wants you involved.

Empower needs almost no ongoing effort. Everything syncs automatically.

Categorization happens automatically.

Your dashboard updates constantly. If time is your scarcest resource, this difference matters.

| Feature | YNAB | Personal Capital (Empower) |

|---|---|---|

| Monthly Time Required | 20-30 minutes | 5-10 minutes |

| Budgeting Approach | Zero-based, proactive | Basic targets, reactive |

| Investment Tracking | Basic balance tracking | Detailed analysis and fee detection |

| Best For | Variable income, active budgeters | Wealth building, passive tracking |

| Price | $109/year or $14.99/month | Free (wealth management optional) |

| Learning Curve | Steeper, needs methodology shift | Minimal, intuitive dashboard |

Performance Analysis: How They Work in Real Life

The automated syncing solves one major pain point from manual tracking. Both platforms connect many bank accounts and credit cards into one place.

You’re not logging into five different websites to see your finish financial situation.

But they handle the data differently.

YNAB’s strength comes from forcing clarity. Because you look at every transaction during the budgeting process, you see exactly where money goes.

This becomes especially valuable when tracking many income sources (critical for freelancers) or identifying subscription services that slowly drain your accounts.

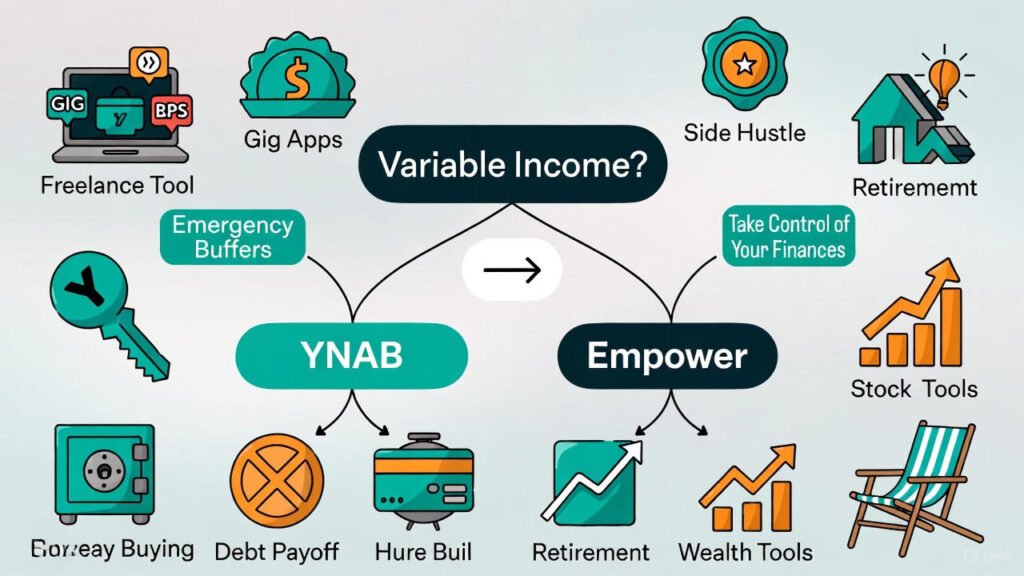

The variable income feature specifically helps people with inconsistent paychecks. Instead of panicking during lean months, you’re building buffers during good months.

You’re essentially living on last month’s income, which creates stability.

Empower handles the bigger financial picture better. You see how your business income flows into personal wealth building.

You understand how your investment allocation affects retirement timing.

You know whether you’re actually on track for financial independence.

The retirement planner runs projections based on your current savings rate, investment performance, and spending patterns. It shows you what happens if you increase contributions by 5% or retire three years earlier than planned.

For couples managing shared finances, YNAB’s separate budget capability let’s both partners see exactly how household money gets allocated. There’s transparency without the need for constant check-ins. Empower’s centralized dashboard shows the combined picture without that spending-level detail.

Price Comparison: Understanding the Real Cost

YNAB costs $14.99 monthly (totaling $179.88 annually) or $109 if you pay upfront for the year. You get a 34-day free trial to test whether it works for your situation.

Empower is free for the dashboard and basic budgeting features. The paid wealth management services cost 0.49% to 0.89% of assets under management annually.

This only becomes expensive if you opt into that service.

The calculation gets interesting when you consider indirect costs.

If YNAB helps a freelancer stabilize irregular income and avoid overdraft fees, that $109 annual cost pays for itself immediately. If the system helps you identify and cancel $15 in monthly subscriptions you forgot about, you’ve covered most of the annual cost.

If Empower’s fee analyzer identifies $2,000 in annual investment fees you didn’t know existed, the free tool just created significant value. If the retirement planner shows you that increasing your 401k contributions by 2% gets you to retirement five years earlier, that insight is priceless.

The “cheapest” option isn’t always the one with the lowest sticker price.

Best For Different Users: Matching Tools to Lives

Variable Income Earners

Your income changes dramatically from month to month. You need to see which months cover basic operating expenses, which can go toward tax reserves, and which build your emergency fund.

YNAB’s “Age Your Money” concept creates a buffer that eliminates feast-or-famine stress. You’re essentially spending last month’s income instead of this month’s.

Variable income management is where YNAB shows clear advantages over other personal finance tracking tools.

Set up separate categories for tax obligations, business operational reserves, and personal discretionary spending. After a high-income month, you’re building stability for lean periods instead of wondering where everything went.

Couples and Families

You need transparency without creating friction. When one partner handles most spending, the other should see clearly where family money goes.

Not to micromanage, but to understand the household financial reality.

Empower’s centralized dashboard showing total net worth, debt progress, and goal status works well here. Some couples use YNAB for detailed cash flow planning and Empower for overall position tracking.

The platforms complement each other if you want both approaches.

Recent Graduates

You’re transitioning from student finances to independent adult money management. You need a system that teaches solid habits while you’re establishing them.

YNAB’s methodology forces intentional spending decisions. This creates discipline early.

The 34-day trial removes the commitment risk.

You can test whether the hands-on approach fits your personality before paying anything.

If you realize you prefer automation over engagement, you can switch platforms without losing much time or money.

Wealth Builders and Investors

You’ve moved past basic expense tracking. You’re optimizing long-term wealth now.

Your priorities are portfolio allocation, fee minimization, and retirement planning accuracy.

Empower’s investment tools, retirement planner, and fee analyzer directly address these needs. The platform won’t replace a financial advisor, but it creates the foundation for better independent decisions.

The Investment Checkup can identify allocation problems that might delay your financial independence by years. The fee analyzer shows you exactly what you’re paying in expense ratios, advisory fees, and fund costs.

Final Recommendation: Making the Practical Choice

Start with your income stability.

If your income varies significantly month to month, YNAB’s paid plan pays for itself through improved financial stability. The $109 annual investment prevents the financial stress and poor decisions that cost far more than the subscription.

If your income is stable and predictable, and your primary concern is investment optimization, Empower’s free dashboard makes more sense. Add the optional paid advisory services only if you need professional management.

For most people, the limiting factor isn’t money. It’s choosing the tool that matches how you actually think about finances.

Someone who makes decisions through detailed analysis will succeed with YNAB. The hands-on approach feeds that decision-making style.

Someone who prefers big-picture visualization and minimal daily involvement works better with Empower.

You can also use both. Some people budget monthly cash flow in YNAB while tracking overall wealth position in Empower.

The platforms serve different purposes, so combining them isn’t redundant if you value what each provides.

The tool you choose matters less than the tool you’ll actually use consistently. Both platforms solve the core pain points.

They eliminate manual tracking burden.

They sync many accounts automatically. They turn raw transaction data into actionable insights.

YNAB gives you spending control and budget discipline. Empower gives you wealth visibility and investment optimization.

Pick based on which problem you’re actually trying to solve.

If you’ve tried automated personal finance tracking tools before and abandoned them because too much felt overwhelming, start with Empower’s simpler approach. If you’ve tried budgeting apps that didn’t create real behavior change, YNAB’s hands-on methodology might be what you need.

The right choice depends on whether you want to actively manage every dollar or passively watch your overall financial health. Both approaches work.

They just work for different types of people with different financial situations and goals.

Pick the one that matches how you actually live, not the one that sounds better in theory.